Mathematics, 13.08.2020 23:01, nathaliapachon7948

You roll a die. If it comes up a 1 or 2, you win $200. If not, you get to roll again. If you get a 1 or 2 the second time, you win $100. If not, you lose. a) Create a probability model for the amount you win. b) Find the expected amount you'll win.

Answers: 3

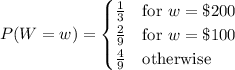

be a random variable representing the winnings from playing the game. It has the probability mass function

be a random variable representing the winnings from playing the game. It has the probability mass function

![E[W]=\displaystyle\sum_w w\,P(W=w)=\$200\cdot\frac13+\$100\cdot\frac29+\$0\cdot\frac49\approx\$88.89](/tpl/images/0721/8069/930b4.png)

Other questions on the subject: Mathematics

Mathematics, 21.06.2019 16:30, 2alshawe201

You are remodeling your kitchen. you’ve contacted two tiling companies who gladly told you how long it took their workers to tile of a similar size jim completed half the floor in 8 hours. pete completed half of the other floor in 7 hours. if pete can lay 20 more tiles per hour than jim, at what rate can jim lay tiles

Answers: 3

Mathematics, 21.06.2019 20:00, smariedegray

Aubrey read 29 books and eli read 52 books what number is equal to the number of books aubrey read?

Answers: 1

Mathematics, 21.06.2019 20:10, morgantisch25

A. use the formula for continuous compounding with the original example: $1000 invested at 2% for 1 year. record the amount to 5 decimal places. use a calculator. b. compare it to the result using the original compound interest formula with n = 365 calculated to 5 decimal places. which has a larger value? explain.

Answers: 1

Do you know the correct answer?

You roll a die. If it comes up a 1 or 2, you win $200. If not, you get to roll again. If you get a 1...

Questions in other subjects:

English, 23.07.2019 09:00

Mathematics, 23.07.2019 09:00

Mathematics, 23.07.2019 09:00

Mathematics, 23.07.2019 09:00