Business, 27.03.2020 22:51, lileljusto2829

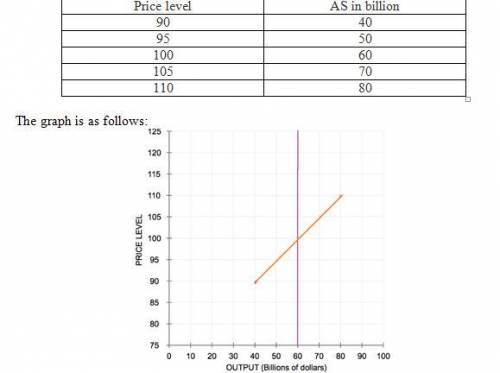

In the short run, the quantity of output that firms supply can deviate from the natural rate of output if the actual price level in the economy deviates from the expected price level. Several theories explain how this might happen. For example, the sticky-price theory asserts that the output prices of some goods and services adjust slowly to changes in the price level. Suppose firms announce the prices for their products in advance, based on an expected price level of 100 for the coming year. Many of the firms sell their goods through catalogs and face high costs of reprinting if they change prices. The actual price level turns out to be 90. Faced with high menu costs, the firms that rely on catalog sales choose not to adjust their prices. Sales from catalogs will (Remain the same/fall/rise), and firms that rely on catalogs will respond by (Increasing/Reducing) the quantity of output they supply. If enough firms face high costs of adjusting prices, the unexpected decrease in the price level causes the quantity of output supplied to (Fall below/Rise above) the natural rate of output in the short run. Suppose the economy's short-run aggregate supply (AS) curve is given by the following equation:Quantity of output supplied = Natural Rate of output + a x (Price level (actual) - Price level (expected))The Greek letter a represents a number that determines how much output responds to unexpected changes in the price level. In this case, assume that a= $2 Billion. That is, when the actual price level exceeds the expected price level by 1, the quantity of output supplied will exceed the natural rate of output by $2 billion. Suppose the natural rate of output is $60 billion of real GDP and that people expect a price level of 100.The short-run quantity of output supplied by firms will rise above the natural rate of output when the actual price level (rises above/falls below) the price level that people expected.

Answers: 3

Other questions on the subject: Business

Business, 22.06.2019 23:20, fedora87

Assume a competitive firm faces a market price of $60, a cost curve of c = 0.003q^3 + 25q + 750, and a marginal cost of curve of: mc = 0.009q^2 + 25.the firm's profit maximizing output level (to the nearest tenth) is , and the profit (to the nearest penny) at this output level is $ will cause the market supply to (shift right/shift left). this will continue until the price is equal to the minimum average cost of $

Answers: 2

Business, 23.06.2019 02:00, rohan13

Opportunity cost is calculated by which of the following? a. adding the value of all lost opportunities. b. subtracting all costs from the total benefit. c. calculating the cost of time, energy, and sacrifice. d. finding the value of the best option that is not chosen.

Answers: 1

Business, 23.06.2019 02:40, dooderh

James sebenius, in his harvard business review article: six habits of merely effective negotiators, identifies six mistakes that negotiators make that keep them from solving the right problem. identify which mistake is being described. the negotiator has neglected to consider the course of action he will take if the proposed deal is not possible.

Answers: 3

Business, 23.06.2019 12:00, Adones7621

The "ideal" business, according to richard buskirk of the university of southern california: has many diverse employees. has a few, carefully selected employees. has many homogeneous employees. is a "one-man show".

Answers: 2

Do you know the correct answer?

In the short run, the quantity of output that firms supply can deviate from the natural rate of outp...

Questions in other subjects:

World Languages, 02.02.2020 06:43

English, 02.02.2020 06:43

Geography, 02.02.2020 06:43

Social Studies, 02.02.2020 06:43

Mathematics, 02.02.2020 06:43

English, 02.02.2020 06:43

English, 02.02.2020 06:43