Business, 10.03.2020 07:57, fraven1819

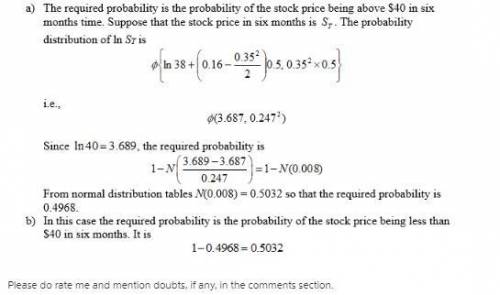

A stock price follows geometric Brownian motion with an expected return of 16% and a volatility of 35%. The current price is $38. a) What is the probability that a European call option on the stock with an exercise price of $40 and a maturity date in six months will be exercised(b) What is the probability that a European put option on the stock with the same exercise price and maturity will be exercised?

Answers: 1

Other questions on the subject: Business

Business, 22.06.2019 00:30, ummmmmmmmmmmm

What are six resources for you decide which type of business to start and how to start it?

Answers: 3

Business, 22.06.2019 05:50, salvadorperez26

Match the steps for conducting an informational interview with the tasks in each step.

Answers: 1

Business, 22.06.2019 10:00, dtaylor7755

How has internet access changed and affected globalization from 2003 to 2013? a ten percent increase in internet access has had little effect on globalization. a twenty percent decrease in internet access has had little effect on globalization. a thirty percent increase in internet access has sped up globalization. a fifty percent decrease in internet access has slowed down globalization.

Answers: 1

Do you know the correct answer?

A stock price follows geometric Brownian motion with an expected return of 16% and a volatility of 3...

Questions in other subjects: